Homeowners Insurance: Complete Guide for 2026

Buying a home is one of the biggest financial investments most people ever make. But protecting that investment is just as important.

That’s where homeowners insurance comes in.

A good homeowners insurance policy can protect you from:

- Fire damage

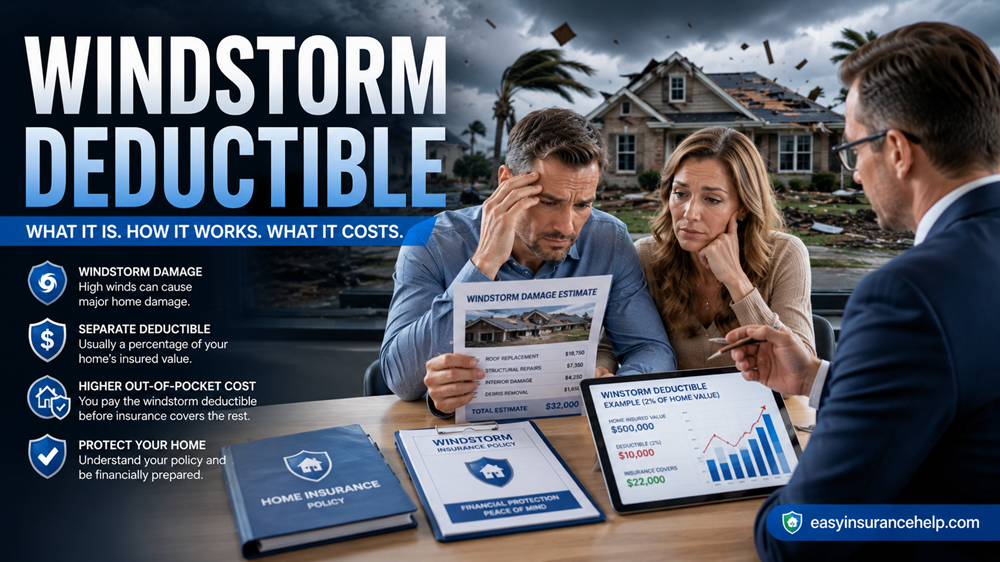

- Storms and natural disasters

- Theft and vandalism

- Liability claims

- Water damage

- Expensive repair costs

Without proper insurance, a single disaster could cost tens or even hundreds of thousands of dollars.

This complete guide explains:

- What homeowners insurance covers

- What it does not cover

- Average insurance costs

- Best homeowners insurance companies

- How claims work

- Tips to lower your premiums

- How to choose the best policy in 2026

What Is Homeowners Insurance?

Homeowners insurance is a property insurance policy that protects your house, belongings, and financial liability.

It helps pay for:

- Home repairs

- Rebuilding costs

- Personal property replacement

- Temporary living expenses

- Legal liability claims

Most mortgage lenders require homeowners insurance before approving a home loan.

What Does Homeowners Insurance Cover?

Most standard homeowners insurance policies include several types of protection.

Dwelling Coverage

Dwelling coverage protects the physical structure of your home.

This includes:

- Walls

- Roof

- Floors

- Garage

- Built-in appliances

Covered events may include:

- Fire

- Windstorms

- Hail

- Lightning

- Explosion damage

Personal Property Coverage

This covers your belongings inside the home.

Examples:

- Furniture

- Electronics

- Clothing

- Appliances

- Jewelry (limited coverage)

If your items are stolen or damaged, insurance may help replace them.

Liability Protection

Liability coverage protects you if someone is injured on your property.

Example situations:

- Guest slips on stairs

- Dog bite incident

- Property damage to neighbors

Liability insurance may cover:

- Medical bills

- Legal fees

- Court settlements

Additional Living Expenses (ALE)

If your home becomes unlivable after a covered disaster, ALE helps pay for:

- Hotel stays

- Food expenses

- Temporary housing

What Homeowners Insurance Does NOT Cover

Many homeowners are surprised to learn standard policies exclude several major risks.

Flood Damage

Flood insurance usually requires a separate policy.

Official information:

FloodSmart.gov

Earthquakes

Most standard policies do not cover earthquakes.

Separate earthquake insurance may be needed in high-risk states.

Normal Wear and Tear

Insurance does not cover:

- Aging roofs

- Maintenance neglect

- Pest infestations

Types of Homeowners Insurance Policies

Different policy forms offer different protection levels.

HO-3 Policy

The most common homeowners insurance policy in America.

Covers:

- Home structure for most risks

- Personal belongings for named risks

Best For

- Most single-family homeowners

HO-5 Policy

Offers broader protection with fewer exclusions.

Best For

- High-value homes

- Maximum coverage needs

HO-6 Policy

Designed for condo owners.

Covers

- Interior structure

- Personal belongings

HO-4 Policy

Also called renters insurance.

Best For

- Apartment renters

Best Homeowners Insurance Companies in 2026

Several insurers consistently rank among the best homeowners insurance providers.

According to Forbes Advisor and J.D. Power rankings, the following companies perform strongly for customer satisfaction and claims service. (forbes.com)

1. State Farm

State Farm is America’s largest home insurer.

Pros

- Strong customer support

- Extensive agent network

- Competitive bundling discounts

Best For

- Nationwide homeowners

2. Allstate

Known for customizable coverage and digital tools.

Pros

- Good mobile app

- Multiple discount options

- Strong optional coverage

Best For

- Tech-friendly homeowners

3. USAA

Available for military members and families.

Pros

- Excellent claims satisfaction

- Affordable premiums

- Strong financial ratings

Best For

- Military families

4. Amica

Highly rated for customer service.

Pros

- Excellent claims handling

- Dividend policies available

Best For

- Customer satisfaction

5. Nationwide

Offers strong replacement-cost coverage options.

Best For

- Flexible policy customization

Average Cost of Homeowners Insurance

Homeowners insurance costs vary based on:

- Home value

- Location

- Crime rates

- Weather risks

- Deductible amount

- Credit history

According to Bankrate, the average homeowners insurance premium in the U.S. continues rising due to inflation and climate-related claims. (bankrate.com)

Average Annual Premiums

| Home Value | Average Annual Cost |

|---|---|

| $250,000 | $1,400–$2,200 |

| $500,000 | $2,000–$3,800 |

| $750,000+ | $3,500–$7,000+ |

States with severe weather risks often have much higher premiums.

Factors That Affect Homeowners Insurance Rates

Location

Areas prone to:

- Hurricanes

- Wildfires

- Tornadoes

- Flooding

usually have higher premiums.

Home Age

Older homes may cost more to insure because:

- Electrical systems may be outdated

- Roofs may be older

- Plumbing risks increase

Credit Score

In many states, insurers use credit-based insurance scores.

Higher credit scores often reduce premiums.

Claims History

Multiple past claims can increase insurance costs significantly.

How to Lower Homeowners Insurance Costs

Here are proven ways to save money.

Bundle Policies

Many insurers offer discounts when combining:

- Auto insurance

- Home insurance

- Umbrella policies

Increase Your Deductible

Higher deductibles usually lower monthly premiums.

Install Security Systems

Security upgrades may reduce risk.

Examples:

- Alarm systems

- Smart locks

- Smoke detectors

- Water leak sensors

Improve Your Roof

Newer roofs often qualify for lower premiums.

Replacement Cost vs Actual Cash Value

Understanding this difference is critical.

Replacement Cost

Pays to replace items at today’s prices.

Better Coverage

- Higher premiums

- More protection

Actual Cash Value

Pays depreciated value after wear and age.

Lower Payouts

- Cheaper premiums

- Less protection

How Homeowners Insurance Claims Work

If damage occurs:

Step 1: Document the Damage

Take:

- Photos

- Videos

- Inventory lists

Step 2: Contact Your Insurance Company

File the claim quickly.

Most insurers allow:

- Mobile app claims

- Online claims

- Phone claims

Step 3: Meet the Adjuster

The insurance adjuster evaluates the damage.

Step 4: Receive Settlement

The insurer pays based on policy terms and coverage limits.

Common Homeowners Insurance Mistakes

Underinsuring the Home

Many homeowners insure based on market value instead of rebuilding cost.

Ignoring Flood Risk

Flood damage is excluded from most policies.

Choosing the Cheapest Policy

Low-cost policies may:

- Limit payouts

- Exclude key protections

- Have poor claims service

Frequently Asked Questions About Homeowners Insurance

Is homeowners insurance required?

Mortgage lenders typically require homeowners insurance before approving loans.

Does homeowners insurance cover roof leaks?

It depends on the cause. Sudden covered damage may qualify, but maintenance issues usually do not.

How much homeowners insurance do I need?

You should have enough dwelling coverage to fully rebuild your home.

Does homeowners insurance cover theft?

Yes, most standard policies cover theft of personal belongings.

What is the best homeowners insurance company?

State Farm, USAA, Amica, and Allstate are frequently ranked among the best insurers in 2026. (forbes.com)

Final Thoughts

Homeowners insurance is one of the smartest financial protections you can buy.

The right policy can protect:

- Your home

- Your savings

- Your belongings

- Your financial future

Before buying a policy:

- Compare multiple insurers

- Review coverage exclusions

- Understand deductibles

- Check replacement cost limits

- Evaluate customer reviews and claims service

A few extra minutes comparing policies today could save you thousands after a disaster.

Internal Link Suggestions

- Best Mortgage Lenders in USA

- Flood Insurance Explained

- Best Home Security Systems

- How to Lower Insurance Premiums

- Renters Insurance vs Homeowners Insurance

Leave a Reply