What Is a Windstorm Deductible in Home Insurance?

If you own a home in a hurricane-prone or high-wind area, you may notice something unusual in your homeowners insurance policy:

A separate windstorm deductible.

Many homeowners are shocked to discover that windstorm deductibles work very differently from standard home insurance deductibles — and they can cost thousands of dollars after a storm.

This guide explains:

- What a windstorm deductible is

- How it works

- Why insurers use it

- States where it’s common

- How percentage deductibles work

- Examples of real claim costs

- Ways to reduce your financial risk

If you live in a coastal or storm-prone region, understanding your windstorm deductible is extremely important.

What Is a Windstorm Deductible?

A windstorm deductible is a special deductible applied to certain wind-related insurance claims.

It usually applies to damage caused by:

- Hurricanes

- Tropical storms

- Named storms

- High winds

- Wind-driven hail

Unlike standard homeowners deductibles that use flat dollar amounts, windstorm deductibles are often calculated as a percentage of your home’s insured value.

How Windstorm Deductibles Work

Most homeowners insurance policies have a standard deductible.

Example:

- $1,000 deductible

But windstorm deductibles are different.

Instead of a flat fee, insurers often use:

- 1%

- 2%

- 5%

- 10%

of your dwelling coverage amount.

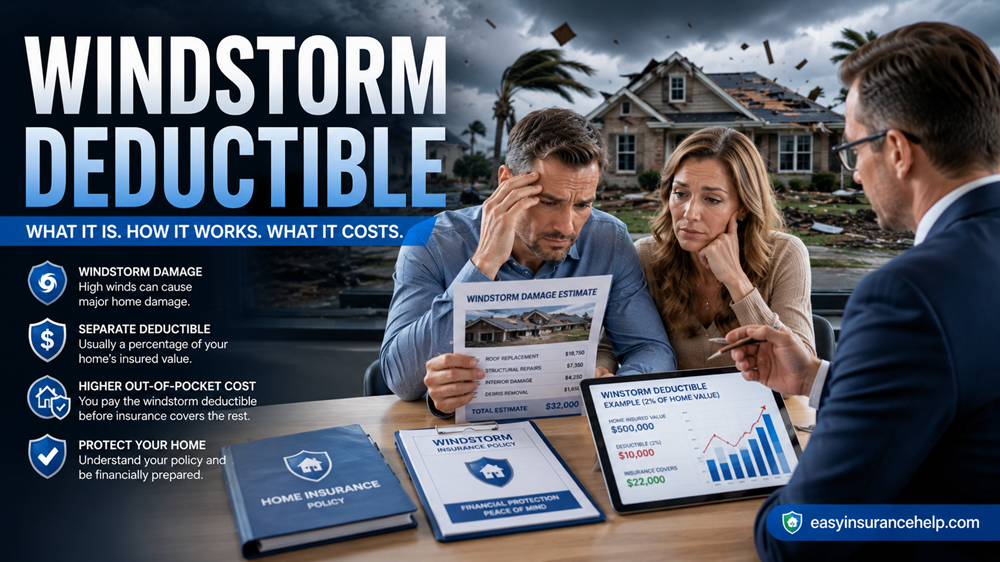

Windstorm Deductible Example

Let’s say:

- Your home is insured for $500,000

- Your windstorm deductible is 2%

Your deductible becomes:

500,000×0.02=10,000

That means:

- You pay the first $10,000

- Insurance pays the remaining covered damage

This surprises many homeowners after major storms.

Why Insurance Companies Use Windstorm Deductibles

Insurance companies use windstorm deductibles because storm claims can become extremely expensive.

Hurricanes and severe storms often cause:

- Roof damage

- Broken windows

- Water intrusion

- Structural destruction

- Widespread regional losses

Windstorm deductibles help insurers:

- Reduce massive payouts

- Control risk exposure

- Keep policies available in high-risk areas

According to the Insurance Information Institute, catastrophe-related losses continue rising significantly across the U.S. insurance market. (iii.org)

States Where Windstorm Deductibles Are Common

Windstorm deductibles are most common in:

- Florida

- Texas

- Louisiana

- Alabama

- Mississippi

- South Carolina

- North Carolina

Some inland states may also use them in hail-prone areas.

Types of Windstorm Deductibles

There are several common types.

1. Hurricane Deductible

Applies specifically to hurricanes.

Usually triggered when:

- National Weather Service declares a hurricane

- Storm warnings are issued

2. Named Storm Deductible

Applies when the storm receives an official name.

Example:

- Tropical Storm Emily

- Hurricane Michael

Named storm deductibles are broader than hurricane deductibles.

3. Wind/Hail Deductible

Applies to:

- Wind damage

- Hail damage

- Severe thunderstorms

Common in:

- Tornado regions

- Hail-prone states

Difference Between Standard and Windstorm Deductibles

| Feature | Standard Deductible | Windstorm Deductible |

|---|---|---|

| Usually Flat Amount? | Yes | Often Percentage-Based |

| Typical Cost | $500–$2,500 | Thousands of Dollars |

| Applies To | General Claims | Wind-related claims |

| Common In | Nationwide | Coastal & Storm Areas |

What Triggers a Windstorm Deductible?

Your policy determines when the deductible applies.

Common triggers include:

- Hurricane warnings

- Named storm declarations

- Wind speed thresholds

- Specific weather events

Always review your policy wording carefully.

Does Windstorm Insurance Cover Flooding?

No.

This is one of the biggest homeowner misunderstandings.

Windstorm coverage usually covers:

- Wind damage

- Roof damage

- Broken windows

But NOT:

- Flood damage

- Storm surge flooding

Flood insurance usually requires a separate policy.

Official information:

FloodSmart.gov

How Much Are Windstorm Deductibles in 2026?

Typical windstorm deductibles include:

- 1%

- 2%

- 3%

- 5%

Higher-risk coastal properties may see:

- 10% deductibles

Windstorm Deductible Cost Examples

Example 1: 1% Deductible

Home insured for:

- $300,000

Deductible:

300,000×0.01=3,000

You pay:

- $3,000 before coverage begins

Example 2: 5% Deductible

Home insured for:

- $700,000

Deductible:

700,000×0.05=35,000

You pay:

- $35,000 out of pocket

This is why understanding your deductible matters.

Why Windstorm Deductibles Increased Recently

Several factors are driving increases nationwide.

Climate Risks

Storm intensity and catastrophe losses continue increasing.

Rising Reinsurance Costs

Insurance companies now pay more for catastrophe protection.

Construction Inflation

Roofing and rebuilding costs are significantly higher in 2026.

More Expensive Claims

Modern homes contain:

- Expensive roofing systems

- Smart technology

- High-end materials

Claims are more costly than ever.

How to Check Your Windstorm Deductible

Review your:

- Declaration page

- Policy deductible section

- Hurricane endorsement

- Wind/hail endorsement

Look for terms like:

- Hurricane deductible

- Named storm deductible

- Wind/hail deductible

Can You Lower Your Windstorm Deductible?

Sometimes, yes.

However:

- Lower deductibles usually increase premiums

- Higher-risk homes may have limited options

You can ask insurers about:

- Alternative deductible structures

- Roof mitigation discounts

- Wind-resistant upgrades

Companies like State Farm, Allstate, and USAA may offer mitigation discounts.

How to Reduce Windstorm Insurance Costs

Upgrade Your Roof

Impact-resistant roofs may qualify for discounts.

Install Storm Protection

Examples:

- Hurricane shutters

- Reinforced garage doors

- Impact-resistant windows

Improve Home Mitigation

Wind mitigation inspections may reduce premiums.

Shop Around

Windstorm pricing varies dramatically between insurers.

Common Homeowner Mistakes

Assuming Deductibles Are Flat Dollar Amounts

Percentage deductibles can become very expensive.

Ignoring Flood Insurance

Windstorm coverage does not replace flood insurance.

Not Reading Policy Details

Many homeowners only discover windstorm deductibles after filing claims.

Frequently Asked Questions

What is a 2% windstorm deductible?

It means you pay 2% of your home’s insured value before insurance covers windstorm damage.

Is a windstorm deductible separate from my normal deductible?

Yes. Windstorm deductibles are usually separate from standard homeowners deductibles.

Does windstorm insurance cover hurricanes?

Usually yes, but hurricane deductibles may apply.

Does windstorm insurance cover flooding?

No. Flood insurance is typically separate.

Can I buy separate windstorm insurance?

Yes. In some high-risk states, separate windstorm policies may be required.

Final Thoughts

Windstorm deductibles are one of the most important — and misunderstood — parts of homeowners insurance.

Unlike standard deductibles, windstorm deductibles are often percentage-based, meaning homeowners may owe thousands after severe storms.

Before storm season:

- Review your policy carefully

- Understand your deductible structure

- Check for flood coverage gaps

- Ask about mitigation discounts

- Prepare emergency savings

Knowing how your windstorm deductible works today can prevent major financial surprises later.

Internal Link Suggestions

- Why Did My Homeowners Insurance Increase So Much

- Flood Insurance Explained

- Hurricane Insurance Guide

- Roof Replacement Cost Guide

- How to Lower Home Insurance Premiums

Leave a Reply